The Beginning Is Always The Hardest

Decentralized Finance (DeFi) came back to life after a dormant few years. The end of 2023 and early 2024 have been generous for protocols’ TVL and its users. Interestingly, the increase in value comes mainly from new projects or protocols developed for years, tapping into fresh trends and narratives. Billions of dollars flowed into liquid staking and liquid restaking. The bright star of this article, Pendle Finance, has been a catalyst for the LRT explosion in Q1 2024. Pendle is a DeFi-native platform to trade the earnings of a crypto asset. It tokenizes the future yield with its distinct PT & YT token design and enables trading strategies.

However, Pendle was not, by any means, an overnight success.

It was founded in 2020 by TN Lee & Vu Nguyen and got little traction initially. The core team has been building its position over the years in DeFi, among yield protocols. Eventually, Pendle witnessed exponential growth in 2024 owing to a tenacious team and versatile approach to markets. They ride the wave of liquid staking and restaking, accumulating over $4B in TVL, a 13x increase since the beginning of 2024, and crossed $15B in cumulative trading volume, a corresponding 35x increase.

Pendle’s co-founders are crypto and DeFi OGs. They contributed to KyberSwap’s development, one of the earliest DeFi protocols. The idea for Pendle emerged during the crypto 2020 summer craze when new food tokens like SushiSwap or PancakeSwap shot left and right, offering +1000% APYs. The team realized it was not sustainable and wanted to create a product that delivered a fixed-rate yield. Therefore, the motivation to start Pendle was to provide fixed-income products to the DeFi community. The mainnet for V1 (version 1) launched on June 17th, 2021, amid last cycle’s bull market pullback. Since then, the team has persisted in developing and improving the protocol despite the bear market in 2022 and the first months of 2023. The launch of V2 introduced redesigned mechanics, facilitating user experience.

Pendle 101: The SY, PT, YT Craze

Pendle’s TVL increase picked up pace after staked ETH withdrawal activation in 2022 and just skyrocketed only with the LRT boom. Pendle benefited greatly from harnessing the potential of emerging narratives, starting with LSTs last year, L2 integrations, and restaking recently.

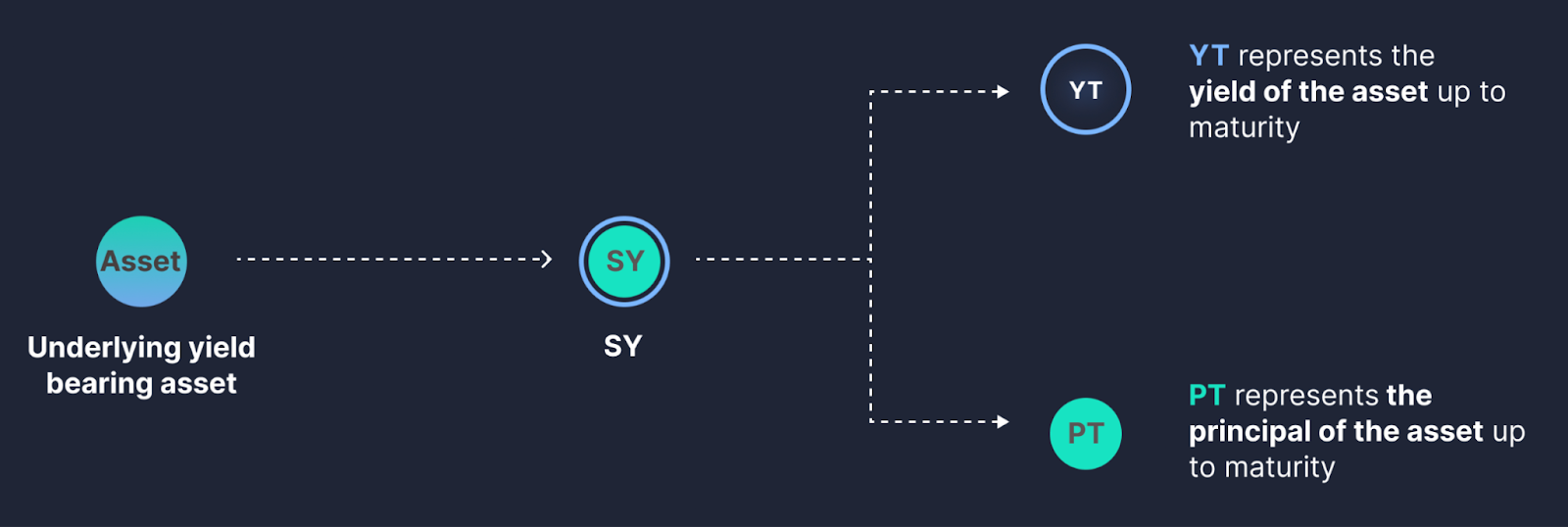

Pendle Finance is a venue for yield trading. The basic mechanics involve splitting the yield-bearing assets like stETH from Lido, sUSDe from Ethena, or weETH from EtherFi into the principal token (PT) and yield token (YT). PT and YT are minted from standardized yield (SY) token standard developed in-house by Pendle. Interestingly, SY is wrapping reward-bearing crypto assets into homogenized form, enabling interactions with a variety of yield-generating mechanisms.

Pendle allows the trading of assets’ Annualized Percentage Yield (APY) component. PT and YT can be traded independently, enriching the DeFi landscape and creating complex and profitable yield strategies. Pendle reduces the opportunity costs associated with DeFi protocol utilization.

Automated Market Maker (AMM) is a big part of the protocol. It is a tailored solution for yield trading focusing on impermanent loss (IL) mitigation. Depositing assets into pools and holding them until maturity ensures a minimal IL. Additionally, liquidity providers on Pendle, breadwinners of DeFi, apart from gaining LP interest, also earn rewards from the underlying protocols of their yield-bearing assets i.e. eETH.

SY token standard ultimately distinguishes Pendle from the other protocols empowering it to transform any yield-bearing asset into principle and yield tokens. Products such as liquid staking tokens (regardless of architecture type, rebasing or reward-bearing), stablecoins, and derivatives can be uniformly converted into PT and YT. The minting process is presented below.

Each PT and YT in the Pendle system has a maturity date. It means that a single asset can have various versions

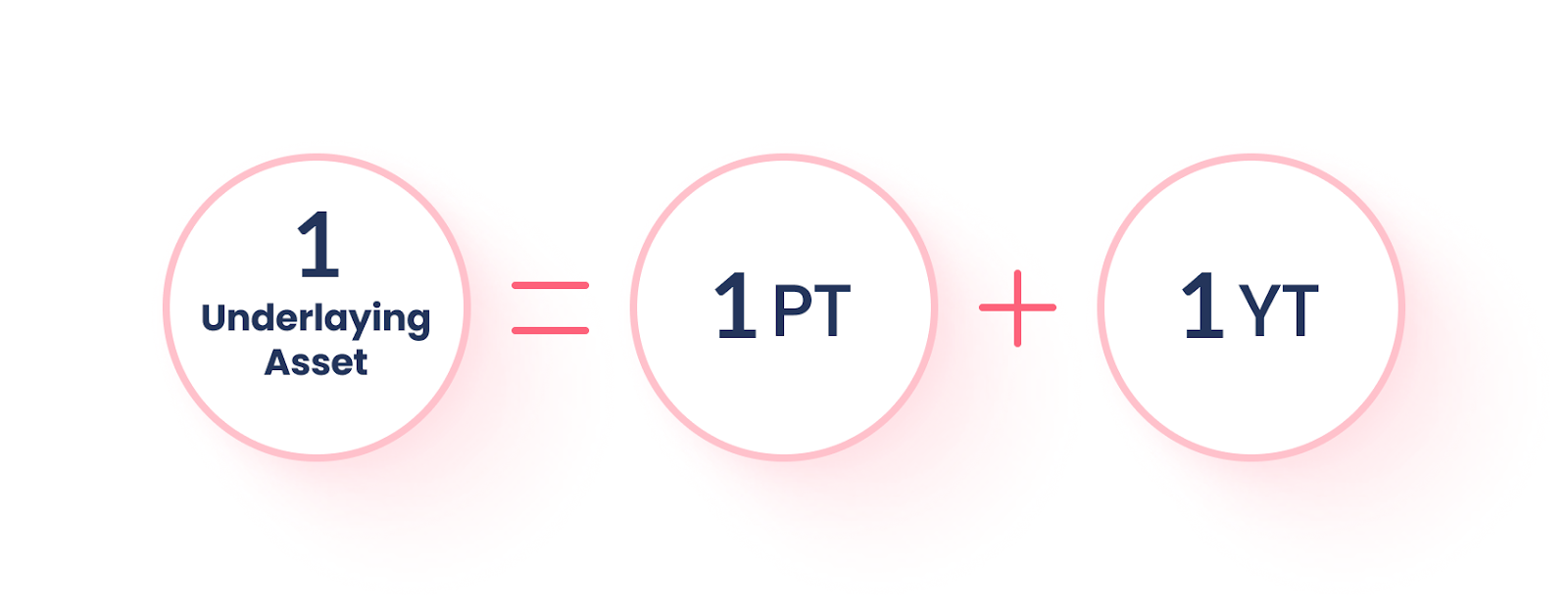

The value of 1 underlying token must equal the sum of 1 PT and 1 YT related to that token. For example, 1 PT-eETH + 1 YT-eETH = 1 eETH worth of weETH on Ether.fi, like in the formula below.

The Principal Token embodies the main fraction of a yield-generating asset. Pendle’s asset-splitting mechanics allow PT to be obtained at a discounted rate compared to the underlying asset due to the separation of its yield component. Remember, 1 PT plus 1 YT equals the underlying asset. Holding a PT until maturity results in a 1:1 exchange ratio for the corresponding underlying token. The predetermined final value of PT, relative to the underlying asset, dictates its Fixed Yield APY. Moreover, PT serves as a fundamental element in all Pendle AMM pools.

The Yield Token represents a reward share associated with a yield-generating asset, entitling holders to receive yield generated by the underlying asset. YT mechanics allow for leveraged exposure without margin or liquidations. Obtaining YT enables one to acquire all the yield from underlying assets. Acquiring YT permits users to open a long position potentially profiting when the yield received surpasses the cost of purchasing YT. The fact worth mentioning is that while at maturity PT is exchangeable for 1:1 the underlying asset, the YT value approaches zero. The same mechanics endure, 1 PT + 1 YT must equal deposited asset.

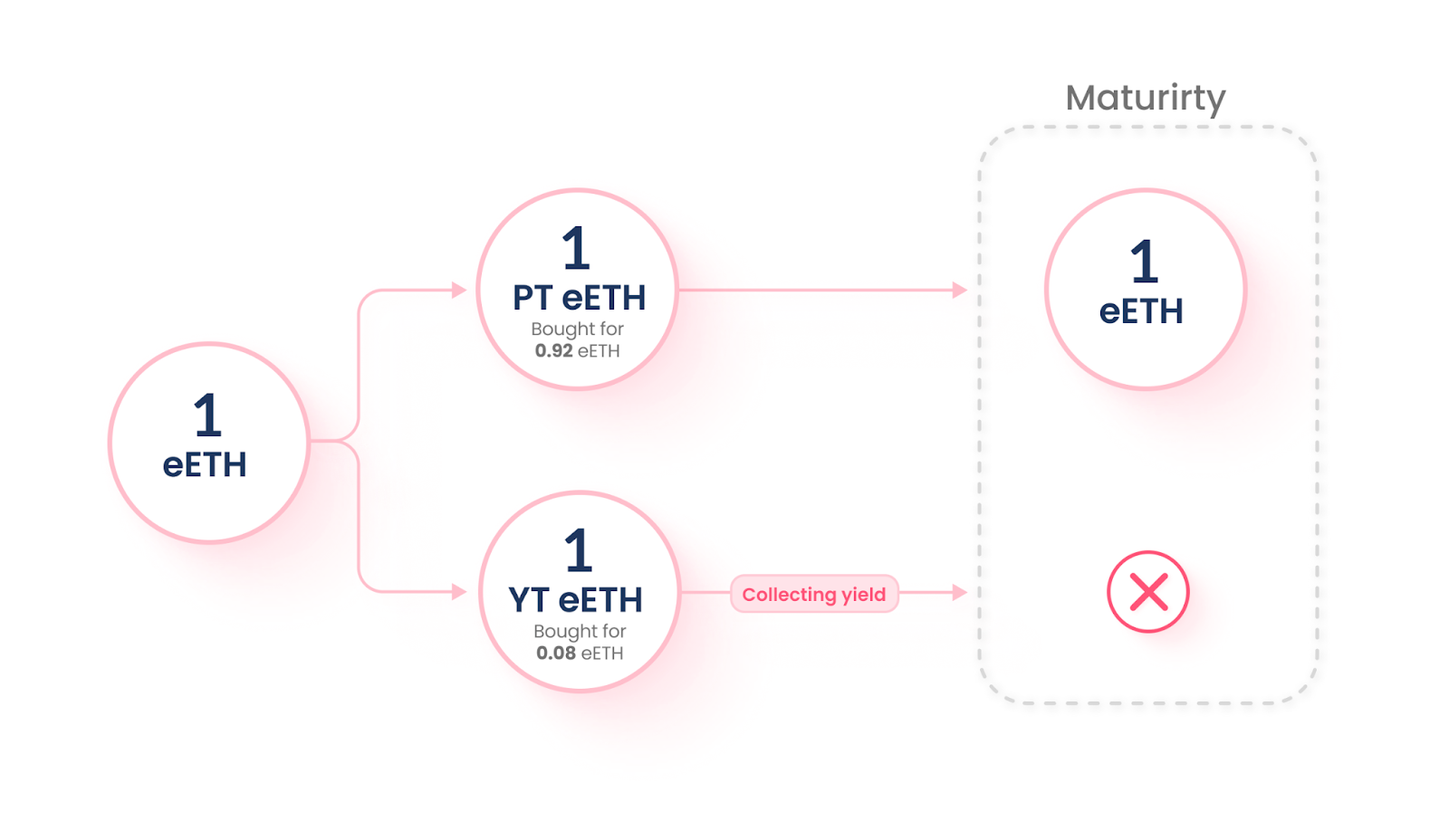

Pendle users can either mint PT and YT or swap their assets for PT or YT independently. Let’s take eETH from EtherFi as an example to mint or swap principal and yield tokens. Graphically, the process is presented below. At current APYs, 1 eETH gives users 1 PT eETH that costs 0.92 eETH and 1 YT eETH that costs 0.08 eETH. At maturity, 1 PT eETH entitles users to redeem 1 eETH, while 1 YT eETH gives users the right to receive the yield of 1 unit of the underlying asset, which is claimable at any time. The YT reaches zero value at maturity as it no longer generates rewards. As time moves towards position expiry, it becomes rational that there is less yield remaining to collect for YT, resulting in its price decrease. Consequently, the lower YT price, leads to an increase in PT price, eventually equaling its underlying value at maturity. Prior to that, PT and YT can be freely traded on Pendle’s marketplace without locks or penalties.

Earn Or Trade: The Beauty of LP Strategies

In principle, Pendle has two protocol modes: Earn and Trade. Pendle Earn is dedicated to less experienced crypto-natives or DeFi users looking for a minimalistic and straightforward yield tokenization process. This mode enables fixed yield and liquidity provisioning. To provide stable returns, Pendle is utilizing its tokenization mechanism and swaps users’ assets for PT. As mentioned previously, PT trades at a discount to the underlying asset, therefore, users’ token value increases at maturity. Referencing our previous example with Ether.fi eETH, when users deposit 1 eETH they receive 1.088 eETH at maturity. Under the hood, users obtain 1.088 PT eETH, which is redeemable at a 1:1 ratio.

But the story does not end there. Pendle enables liquidity provision (LP) to supply its AMM. Providing liquidity to Pendle pools grants depositors rewards from multiple sources: underlying asset APY, PT fixed yield, AMM swap fees, and PENDLE token rewards.

With its V2, Pendle tackled one of the biggest LP issues – impermanent loss (IL), a situation where the price of deposited assets changes compared to when they were deposited.

Their mechanism ensures low IL and near zero or zero IL at maturity. Impermanent loss occurs when pooled assets change in relative price. Pendle mitigates that through high asset correlation thanks to PT/SY pools. Unique AMM design enables PT and YT swaps through a single pool, therefore, liquidity providers can earn fees from both PT and YT swaps.

Now, let’s make things a bit more spicy and dive deeper into Pendle Trade. It is a Pendle platform running in full swing, providing all protocol capabilities. Apart from Pendle Earn use cases, Trade offers more advanced yield-generation opportunities and “degen” trading strategies. Users can expand their operations to YT and reap the benefits of Pendle’s groundbreaking yield tokenization model. Entering Pendle Trade, users encounter the list of available crypto assets with position details. The same token can be listed several times, depending on available maturities. Users can buy PT for a fixed APY and short yield or buy YT to gain rewards and a long position yield. One metric might seem unfamiliar and that is the Implied APY. In short, it measures the value of YT in yield % terms. Implied APY constantly oscillates based on market supply and demand for PT and YT. Decoding its movement is pretty straightforward, PT is cheap and YT is expensive when Implied APY is high and vice versa when it is low.

Obviously, Pendle Trade still retains PT and YT minting and LP. The marketplace enables selling principle and yield tokens independently for an underlying asset, providing users freedom and flexibility. Moreover, Pendle incorporates an interesting feature where users can open limit orders to buy or sell PT and YT, depending on Implied APY.

Points… Points Everywhere

Pendle mastered identifying opportunities and participating in growing trends and narratives. Their strong focus on business development and lightning-fast integration process has contributed to an enormous TVL increase in recent months. One of the most fruitful plays includes enabling points trading and continuous points accrual from protocol assets.

Point campaigns are a thing in 2024 and no wonder they have – in the end, who doesn’t like to earn points? Ethena has had a Shard and Sats campaign, restaking protocols like Ether.fi, Renzo, Swell, Kelp, and Puffer have their own points. Pendle’s yield splitting and tokenization fit right into this madness, providing a venue for yield trading. All these protocols incentivize YT trading with point multipliers. making the Implied APY high. But let’s finish fundamentals, The possible Pendle strategies will be presented further in the article.

Pendle enables point distribution, letting users maintain any airdrop or other incentive rights from integrated projects. Pendle splits the yield-bearing assets like LRTs or stablecoin derivatives into PT and YT where yield tokens accrue all the rewards and points. Partner projects rate Pendle as a valuable ecosystem companion and provide bonus points allocation to incentivize participation.

Pendle And LRTs: TVL Exploding Composition

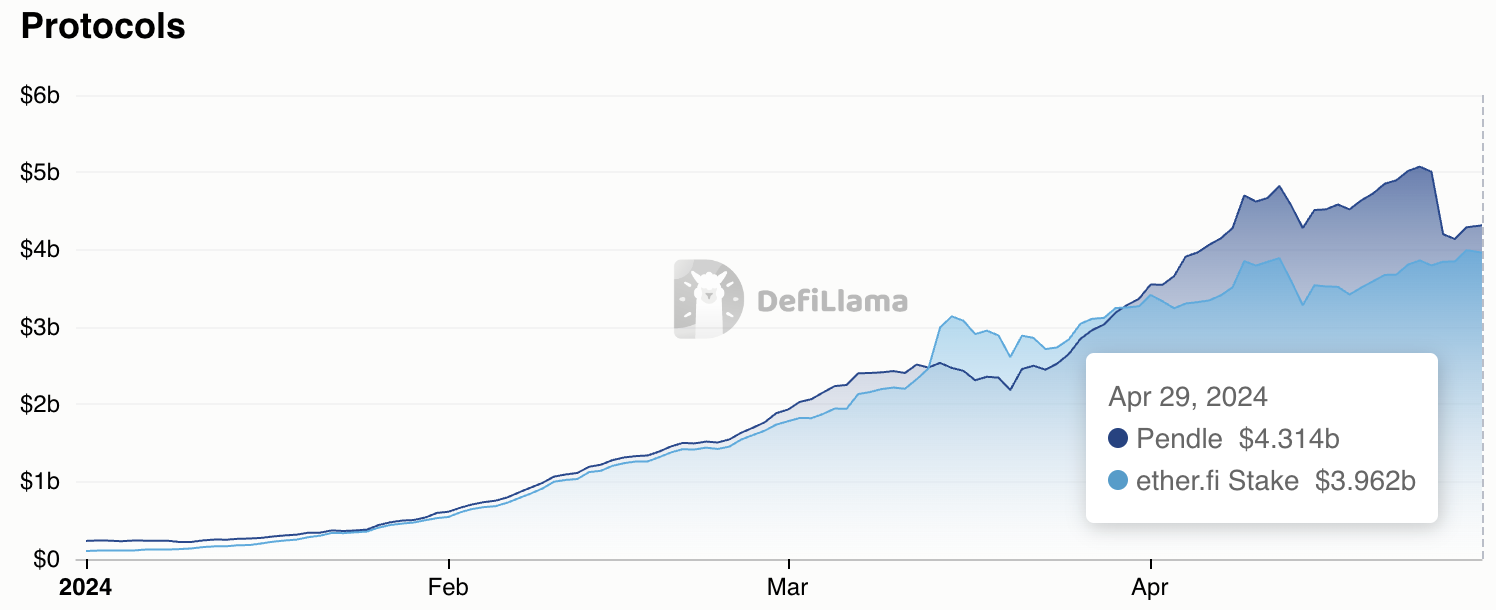

Pendle is unquestionably DeFi top performer regarding TVL and volume gains, and user onboarding in the last months. Its development coincides with liquid restaking category growth. The team was fast tapping into this narrative and answered DeFi users’ needs, integrating the most desirable assets, one of which was eETH from Ether.fi. eETH was integrated at the end of January and since then protocols TVL have risen in parallel. Ether.fi was one of the first projects to introduce LRT and a points program for users. Those two features combined contributed to the popularity of YT trading. Users utilized Pendle leveraged yield exposure by buying YT eETH. Ether.fi was the first protocol to conduct the airdrop campaign and distribute tokens. Users who used Pendle saw rewards increase, setting the path for other protocols, including Kelp DAO and Renzo.

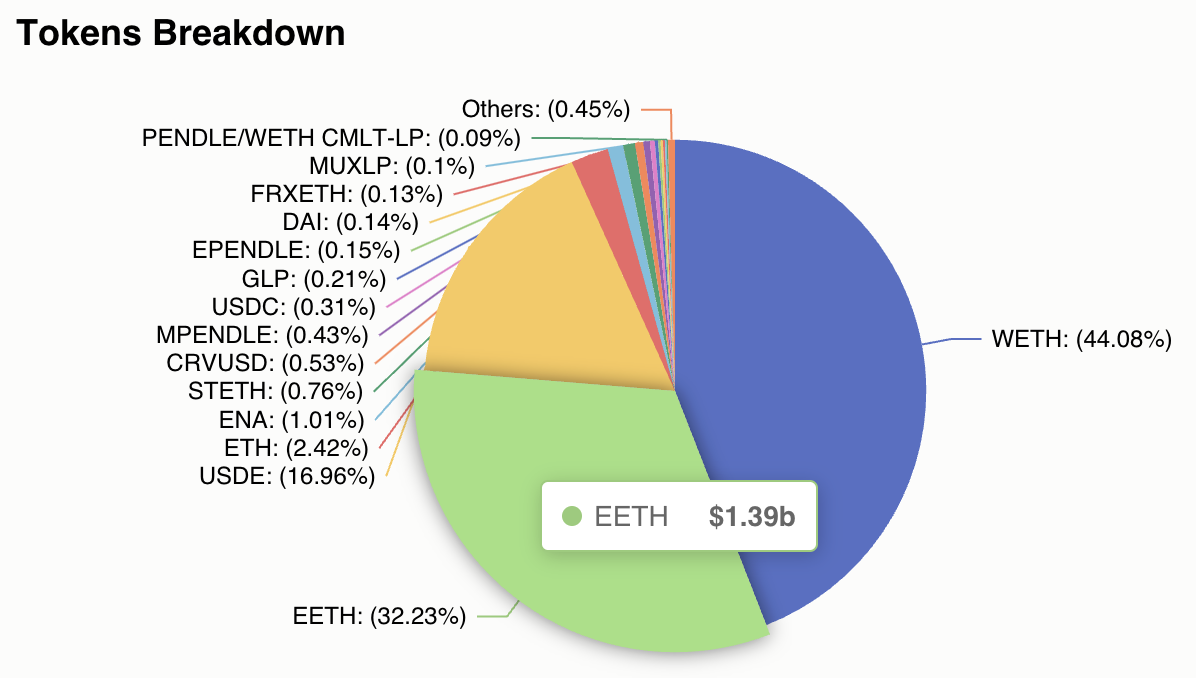

eETH pool (June 2024) on Pendle has by far the largest liquidity, almost double in size compared to the second place ezETH. This can be observed on both Ethereum and Arbitrum networks. The weETH (wrapped eETH) pools on either network regularly topped the daily trading volume metric on Pendle with brief episodes for other LRTs or USDe and recent ezETH domination. eETH accounts for ~32% of tokens deposited into Pendle, which declass other liquid restaking tokens. Pendle’s expansion to Layer 2 undoubtedly injected additional liquidity and brought more users. The external oracles on Layer 2s are required to provide the contract ratio of the accepted yield-bearing assets from Ethereum Mainnet. For that purpose, Pendle uses RedStone Oracles on Arbitrum to source the contract ratio of several markets, including weETH.

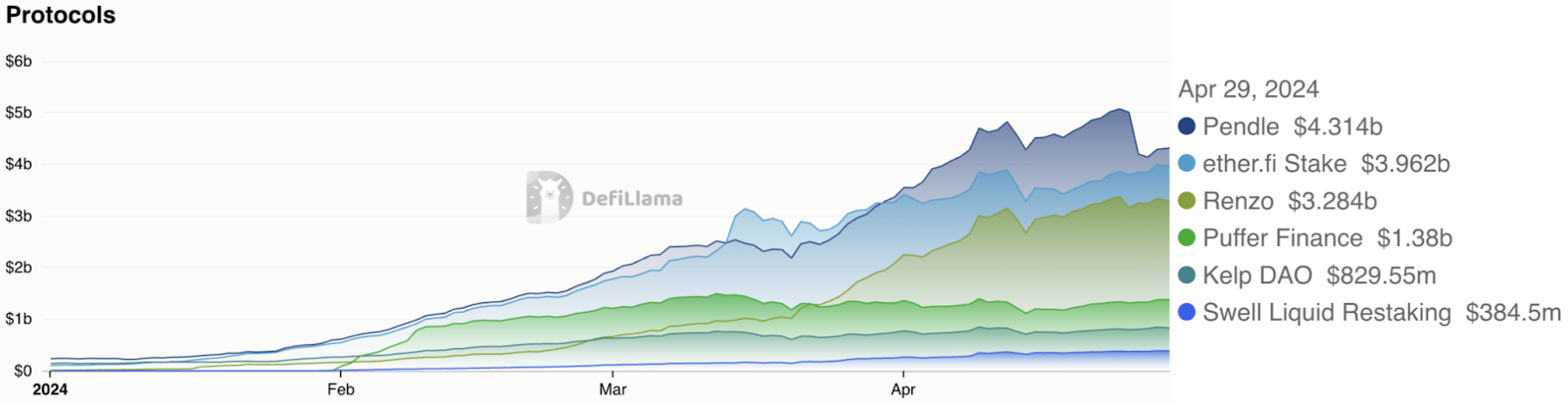

Pendle & Ether.fi TVL Comparison Source: DeFiLlama

Ether.fi is not the only liquid restaking protocol growing jointly in TVL with Pendle. The group includes projects such as Renzo, Puffer Finance, Kelp DAO, and Swell, which better or worse follow Ether.fi trajectory. eETH, rsETH (Kelp DAO), and pufETH (Puffer) were integrated on Pendle almost the same day, on January 25th-27th. eETH is definitely in the front in terms of the accumulated value. However, Puffer and Kelp DAO cannot be diminished, and their numbers are still impressive, crossing the $2B mark together. Renzo had a fantastic April, having the best growth rate. It breathes down Ether.fi’s neck, accruing $3.3B in TVL. Renzo’s popularity is reflected in daily trading volumes as well, being top of the list for the past two weeks. Swell introduced its liquid restaking product later than the competition, initially focusing on liquid staking. The chart below does not do Swell the favor, but TVL close to $400M is definitely not a meager amount. Swell has the potential to catch leading LRT protocols, considering it has the longest-lasting point campaign running and swETH was one of the earliest tokens integrated on EigenLayer.

Non-Financial Advice, Some Most Popular Pendle Strategies in Q2 2024

One of the most popular Pendle strategies is YT trading for LRT protocols. Liquid restaking protocols amassed over $10B with most of the TVL growth in 2024, increasing 35-fold since the beginning of the year. Interest in YT grew due to the various point campaigns and airdrops introduced by protocols. This was the case for Ether.fi and KelpDAO. Users bet on the yield generated by YT to acquire as many points as possible to claim as many airdrop tokens. It is a profitable strategy when the yield produced by the YT becomes bigger than the cost of buying the YT. In addition, increased interest pushes the YT price higher, also providing gains (if sold for capital profits). For example, buying 1 weETH worth of YT eETH gives users exposure to the amount of yield generated by around 7 eETH. That is Pendle’s party trick. It offers users leveraged yield exposure without the risk of liquidation because there is no borrowing. Therefore, anticipated rewards can substantially exceed the standard approach. LRT protocols themselves spice things up, providing point multipliers. This encourages users even more to utilize Pendle and choose its products to maximize yield.

The next prospective strategy can sort of result from the previous one. The strong demand for YT squeezes its price higher. Remembering the principle equation that 1 YT + 1 PT = 1 underlying asset, while YT price increases, PT value decreases. This situation provides a potentially profitable trade opportunity where users can buy PT at a discount. The divergence can be noticeable at times. Taking eETH as an example and the Dec 2024 contract, users can swap 1 eETH for 1.19 PT eETH. At maturity, PT holders receive 1:1 of the underlying asset, cashing in a hefty fixed yield. The profits depend on the supply and demand of YT and PT which is reflected in the Implied APY. As the Implied APY increases, the price of YT rises and the cheaper the PT is. The recent YT trading popularity disclosed several lucrative PT trades. Both strategies are not only applicable to LRTs. Ethena’s USDe has massive traction on Pendle as well. Similarly, Ethena conducted the Shards Campaign to onboard ETH as a backing asset and currently carries out the Sats Campaign to introduce BTC as USDe collateral. Users still buy YT expecting airdrop tokens. As a result, USDe has an attractive fixed yield for PT USDe, considering that it is a stablecoin.

Pendle’s yield tokenization mechanism lets users short or long yield. The split of the yield-bearing asset into the PT and YT enables new trading strategies. The first method where users double down on YT is a long yield exposure. This strategy is profitable when the Implied APY increases, the underlying APY rises, and anticipated rewards (points and/or airdrops) surpass the cost of buying YT. It is worth acknowledging that, akin to most investments, higher potential rewards entail higher risks. When the Implied Yield significantly exceeds the Underlying APY, the Long Yield APY turns negative. Purchasing YT might cost more than the average future yield collected, deeming YT purchase unfavorable. Ultimately, by entering a long-yield position, your profitability hinges on the sustained or increased yield.

The latter strategy can be described as a yield shorting. Obtaining only PT exposure forfeits any rewards. Acquiring PT serves a dual purpose beyond simply generating a fixed income. It also functions as a means to speculate on declining yields. When market sentiment anticipates a decrease in yield, the price of PT rises, effectively positioning PT as a bet against declining yields. Thus, PT also represents a short-yield position. The effect is a discount on PT relative to the underlying asset.

Looking Ahead: Ethena and Cross-chain Expansion

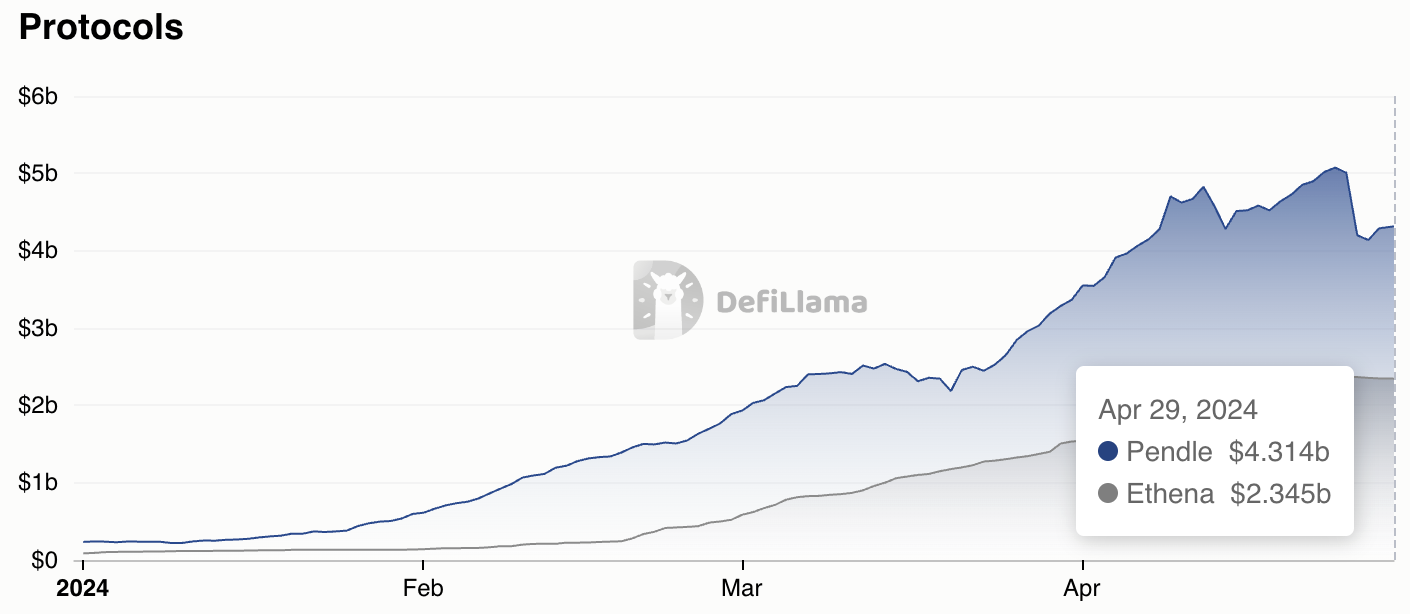

Pendle’s growth is impressive and the praise falls for world-class business development and integration teams. Pendle is always on top of the emerging narratives and trends. Liquid restaking and the USDe launch contributed to the protocol’s popularity. Stablecoin from Ethena, USDe, was one of the biggest drivers in Pendle’s expansion. Ethena itself witnessed a tremendous growth. More on them can be read in our article about Ethena.

Together with the shard campaign from Ethena, Pendle introduced a USDe pool. This brought new users who wished to maximize their returns while still being eligible to earn shard rewards. Ethena guaranteed point multipliers to incentivize users’ participation through Pendle further. Points mania did not stop there. The following Sats Campaign offers 5x to 30x multipliers for Ethena products, including sUSDe, USDe, and ENA. Pendle and Ethena grew together, Pendle in volume and Ethena in TVL. The initial craze for YT USDe created a lucrative opportunity on the other side for PT still offering a fixed yield of 40% APY. The intense traffic resulting from USDe and ENA integrations increased earnings for liquidity providers. Minting SY for Ethena assets is restricted within Pendle, effectively limiting the accumulation of USDe holdings in Pendle contracts. This measure is implemented to forestall any significant surge in USDe supply, following Ethena’s risk guidelines.

Pendle plans do not rely only on new integrations but also on further cross-chain expansion. Pendle protocol is already available on Ethereum, Arbitrum, Optimism, and BNB Chain. Available pools differ depending on the selected network. Respective networks like Arbitrum or BNB Chain have distinct protocols. It introduced the USDe pool on the Mantle network. Users can trade PT and YT, or provide liquidity to earn sats and EigenLayer points. The multiplier also works on Mantle. Recently integrated or less popular networks usually have higher APYs for the same asset. In such cases, users can increase their returns just by bridging their assets.

About RedStone

RedStone is a modular oracle delivering diverse, high-frequency data feeds to EVM Layer1, Layer2, Rollup-as-a-Service networks, and beyond, i.e., Starknet, Fuel Network, or TON. By responding to market trends and developer needs, RedStone can support assets not available elsewhere. The modular design allows for data consumption models adjusted to specific use cases, i.e., capital-efficient LSTfi and early support of LRTs. RedStone raised almost $8M from Lemniscap, Blockchain Capital, Maven11, Coinbase Ventures, Stani Kulechov, Sandeep Nailwal, Alex Gluchovski, Emin Gun Sirer, and other top VCs & Angels.