First Things First: What Is Restaking And EigenLayer?

In the realm of distributed systems like blockchains, we often encounter the Cold Start Problem.

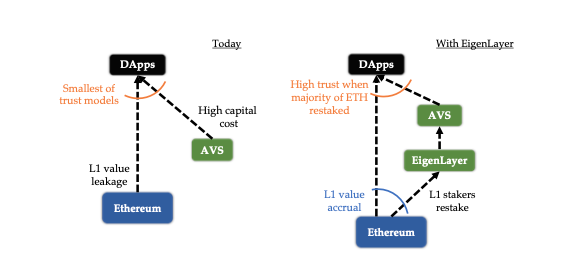

Namely, the problem of enough economic incentive and network effect to secure a new system. Especially, compared to Ethereum’s distributed validator network. This is where the concept of restaking comes into play, creating a market for Ethereum’s validation trust. This involves repurposing the bonded asset, the natively or liquid staked Ether, to empower external systems like rollups, RPCs, data availability, oracles and more with the economic security layer. At the forefront stands EigenLayer with its vision for increasing capital efficiency of the staked assets and machines used for Ethereum staking. However, with great power comes great responsibility. A gradual and prudent implementation of staking is essential, as the stakes are far greater than ever before.

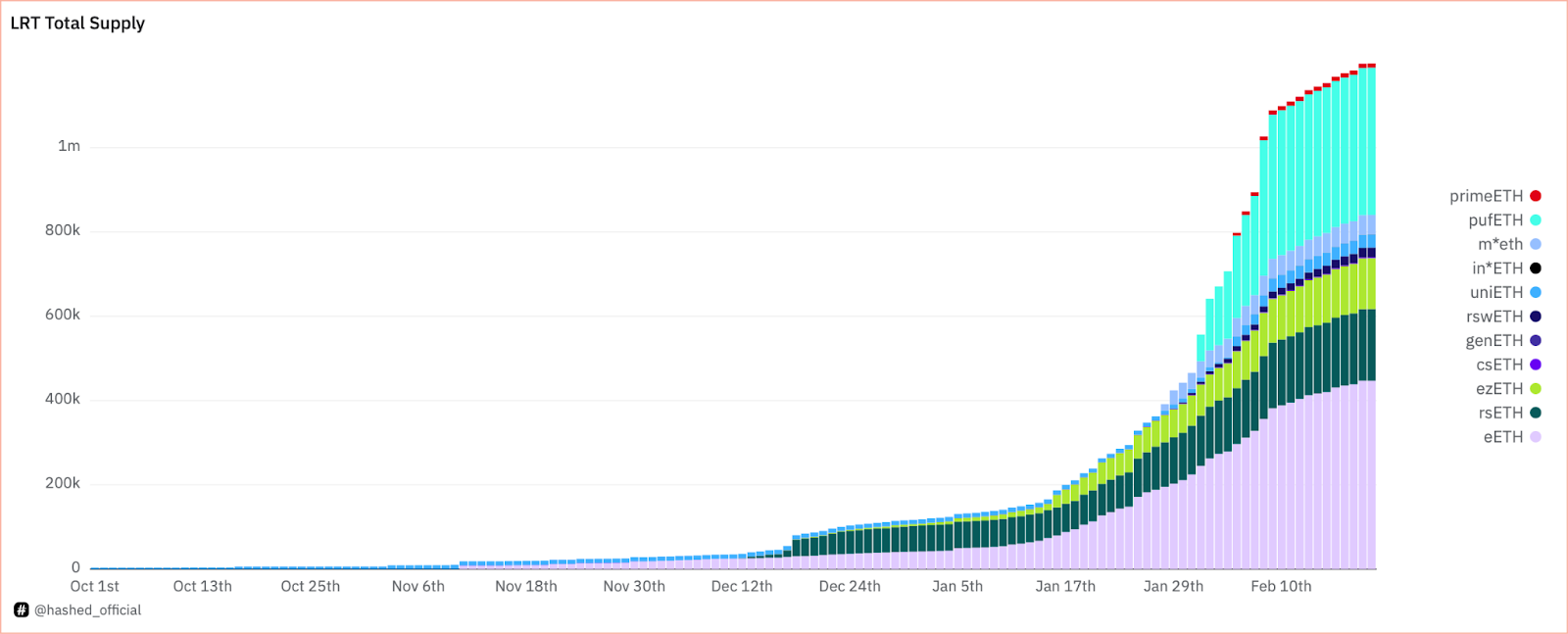

Notably, by 20 February 2024, the Total Value Locked (TVL) in EigenLayer amounts to 7.6 Billion USD (2.6 Million ETH) and TVL in the Liquid Restaking category 3.5 Billion USD.

EigenLayer stands as the undisputed frontrunner and innovator in the restaking domain. Founded by Sreeram Kannan, an Associate Professor at the University of Washington, drawing upon his academic research for the foundational idea. The company has successfully raised over $65M in funding from leading crypto venture capital funds by 2023. EigenLayer has undoubtedly clinched the top spot as the hottest topic in the crypto world at the start of 2024. Numerous new projects, designed to support the growth of the EigenLayer ecosystem and often distinguished by their innovative point systems, are sprouting rapidly. While the EigenLayer narrative is widely discussed from various angles in the crypto community, there seems to be a recurring oversight by the general audience about the core concept of Restaking and its potential to revolutionize the field.

In a nutshell: what is EigenLayer all about?

“EigenLayer is a protocol built on Ethereum that introduces restaking, a new primitive in cryptoeconomic security. This primitive enables the reuse of ETH on the consensus layer. Users that stake ETH natively or with a liquid staking token (LST) can opt-in to EigenLayer smart contracts to restake their ETH or LST and extend cryptoeconomic security to additional applications on the network to earn additional rewards.” Source: EigenLayer docs

EigenLayer, while complex and multifaceted, can fundamentally be described as a general-purpose, dual-sided marketplace for decentralized trust. It’s built atop Ethereum, arguably the most extensive programmable decentralized trust network, and it effectively separates Ethereum’s trust layer, allowing its components to be redeployed for various purposes. The structure of EigenLayer places a strong emphasis on its two-sided nature, which includes:

- Actively Validated Services (AVS) – Any system that requires its own distributed validation semantics for verification, forms the demand side of the EigenLayer marketplace. This includes a diverse array of technologies and platforms, such as sidechains, data availability layers, new virtual machines, keeper networks, oracle networks, bridges, threshold cryptography schemes, and trusted execution environments.

- Restakers – Users who either stake ETH natively or use a liquid staking token (LST) and opt into EigenLayer’s smart contracts for restaking. They form the supply side of the EigenLayer marketplace. By doing so, they extend crypto-economic security to additional applications on the network and, in turn, earn extra rewards.

Source: EigenLayer Whitepaper

It’s also crucial to note that EigenLayer aims to introduce free market dynamics into this scheme. Ideally, this means that no single entity holds a majority of power over either side of the supply and demand equation.

Within the two primary categories of EigenLayer, there’s another key actor known as the Operator. An Operator is an entity responsible for running the software developed on top of EigenLayer. Operators register with EigenLayer, enabling stakers to delegate to them and choose to offer various services built upon EigenLayer. Operators can also be stakers, with no inherent conflict between the two functions.

Below is a list of some organizations that have already registered to serve as operators within the EigenLayer ecosystem:

Note: This list comprises solely vanilla EigenLayer operators, which refers to entities that have chosen to support native staking directly, without the use of intermediaries. LRT Protocols, as extensively covered in this report, may either manage their operator setups or entrust these operations to distinct, specialized third-party providers.

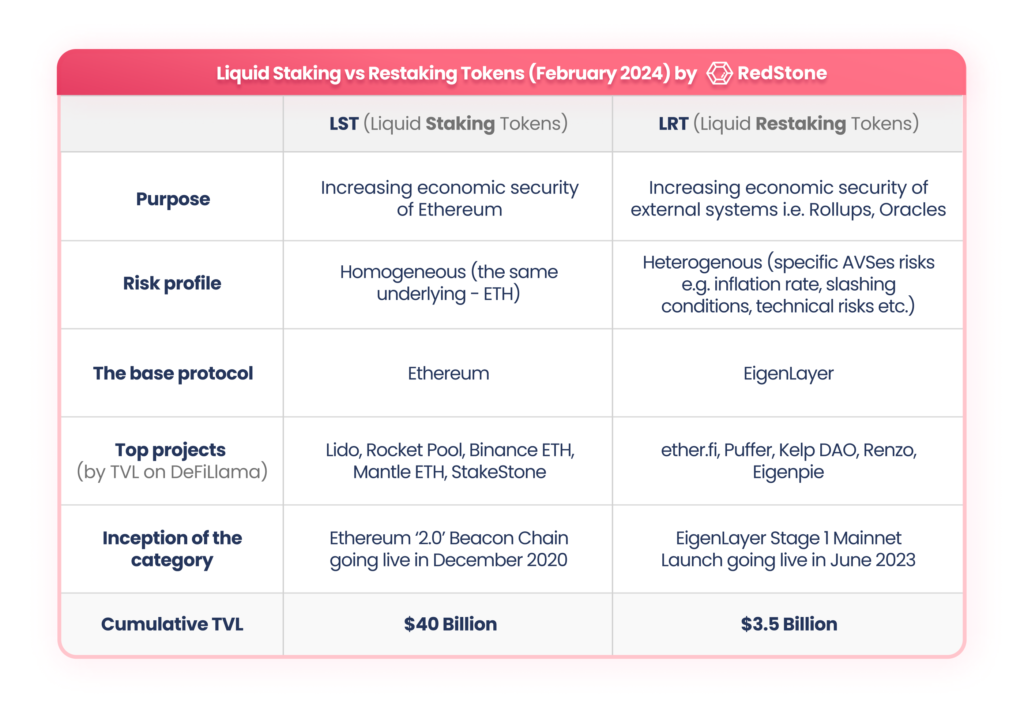

Understanding that EigenLayer is an extension of Ethereum staking, we can deduce why there is an essential need for the liquid restaking landscape and, consequently, Liquid Restaking Tokens (LRT). We’re all familiar with the convenience offered by liquid staking protocols, and we’ve come to recognize that operating a validator is not a straightforward task. However, there are numerous, distinct market dynamics that position LRTs as a crucial component of the restaking puzzle.

Liquid Restaking Tokens (LRTs): What Are They And Why Do They Matter?

So, starting from the first principles, let’s delve into the arguments that underscore the importance of Liquid Restaking Protocols and, by extension, Liquid Restaking Tokens:

A safety buffer: A key characteristic of LRTs is their role as a buffer between Ethereum Mainnet and the risks linked to permissionless AVSs. Should a node operator face liquidation due to malicious activities or an inactivity leak, there’s no immediate requirement to withdraw Ether from the Beacon Chain. Instead, LRT tokens change hands, presenting a much lower risk of a liquidation cascade. It’s important to note that Ethereum Beacon Chain withdrawals are always an option, but in this market structure, they primarily act as a secondary line of defence. Another vital factor is the diminished volatility in EigenLayer security, which, in turn, contributes to the stabilization of Ethereum’s base layer security.

Another chance to strive for the vitality of Ethereum staking: Liquid restaking protocols, an evolution of the conventional liquid staking market, by this extent, the table stakes task for restaking protocols is to participate in the Ethereum consensus. This phenomenon grants Ethereum an additional chance to democratize the staking space, challenging the dominance of the established liquid staking giants.

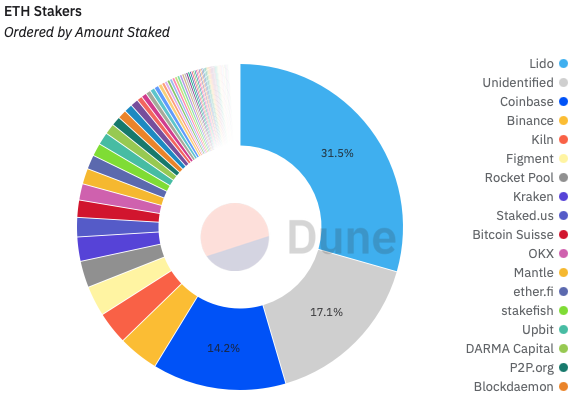

Source: Hildobby’s Ethereum Staking Dashboard

Simplicity: Familiar with the convenience of Liquid Staking protocols, we all got to understand that operating a validator is not a simple endeavour: managing the infrastructure, monitoring its status, and handling potential downtime failures demand somewhat of technical knowledge. This very logic also applies to LRT protocols, as they handle all the restaking technicalities behind the scenes, thus removing the complexity for the end user.

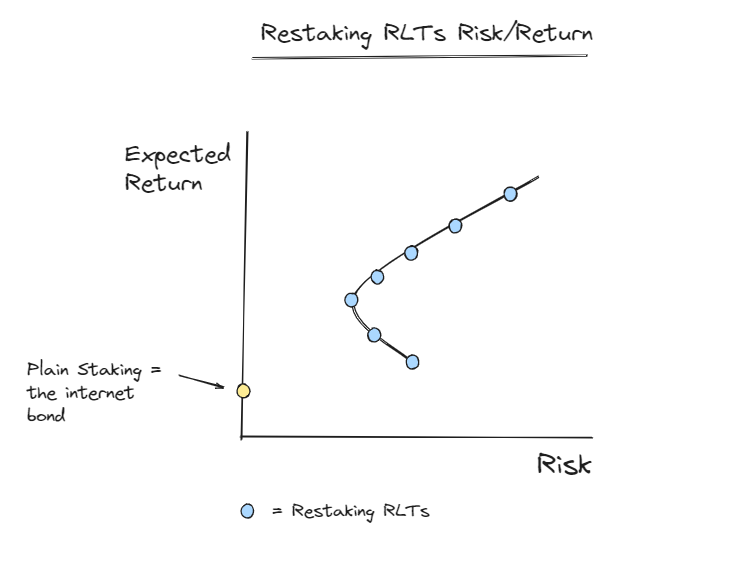

Risk Management: Again referring to the common knowledge about the Liquid Staking Protocols, it’s clear that the supply chain of LRTs is significantly more nuanced. To put it in perspective, all LSTs are doing the same job – validating Ethereum consensus. However, when it comes to LRTs you can do as many jobs as you’d like (as per market demand for restaking-based middleware), but they’ll have severely distinct risk profiles. Meaning, each LRT might have a different yield and a different risk level, because each one of them holds a unique restaking combination. So, generally, we introduce another dimension to the staking equation – knowledge about the technical and financial risks each AVS presents and the capability to quantify them – making it an order of magnitude more complex than good old liquid staking.

Source: Idan Levin

Appetite for higher ETH Yield: Given the steady increase of ETH staked in the post-Merge era, the yield from native staking is correspondingly decreasing, a trend showing no signs of abating. Aware of this, there’s a substantial demand for enhanced yields on what is often referred to as the ‘internet bond’ aka staked Ether. The LRT market is best positioned to capitalize on this growing demand.

Availability: Currently, EigenLayer LST deposits are subject to a capping policy. However, there are no caps on native re-staking. Native restaking is what we refer to as solo-staking – depositing 32 ETH into the Beacon Chain contract, running an Ethereum client node, etc., with the minor yet significant addition of integrating with EigenPods – a user-specific contract deployed to handle native restaking. All LRT protocols employing native restaking possess unbounded growth potential.

Gas Efficiency: AVSs are set to distribute countless rewards, not only in ETH but also in a variety of other tokens. This could turn into a highly gas-intensive task on the resource-limited Ethereum L1. In contrast, LRTs have the capability to batch-collect rewards for the entire pool collectively and then distribute them among protocol holders in various efficient ways, thereby conserving user resources.

Taking all these aspects into account, we can fairly surmise that should EigenLayer achieve its projected success, the LRT market will occupy a substantial position in the DeFi and broader crypto ecosystem.

LRTs & Liquid Restaking Protocols You Need To Know About

Now that we’ve set the stage, who exactly makes up the LRT landscape?

We’ve compiled an overview that highlights all Liquid Restaking Protocols, showcasing their advancements and innovations rooted in EigenLayer technology.

Note: This represents just one facet of the EigenLayer market: the restaking supply. We’re not yet addressing the other side of the equation – the demand, so Actively Validated Services (AVSes) in this report. We will prepare the second part for AVSes.

Although many liquid restaking protocols remain in stealth mode, a few have already enabled Mainnet participation for users, including ether.fi, Renzo Protocol and Keplr DAO. It’s also important to highlight that while the Swell LST division has moved well beyond the initial adoption phase and stands as a potential new LST unicorn, its LRT segment featuring the distinct $rswETH derivative has just been launched.

While liquid staking protocols are often lumped together, each one is unique in its approach to establishing a legitimate product-market fit. Here’s a brief overview of the biggest contenders:

- Ether.fi (eETH) – the dominant player with a substantial share of today’s LRT market. Ether.fi is a protocol that, from the outset, seamlessly integrated liquid staking with the restaking offering. Detailed specifics of ether.fi’s staking model is still forthcoming, but it’s known that the platform distinguishes itself through features like non-custodial staking. Here, stakers can encrypt their validator key using the public key of a node operator selected through an auction mechanism, allowing them to retain full control over their deposits. Looking ahead, the team plans to augment this with the Distributed Validator Technology (DVT) schema. Ether.fi is also heavily investing in becoming the go-to institutional restaking solution while staying true to the ethos of decentralization, as evident in their initiatives supporting solo-stakers. Ether.fi offers two versions of its LRT: $eETH with a rebasing structure, and $weETH, a reward-bearing token.

- Kelp DAO (rsETH) – presents a compelling case, notably being founded by Stader Labs, the team behind a successful LST protocol issuing ETHx. Their origins have earned the project an initial vote of confidence from the community. Kelp facilitates LST deposits, backed by an equivalent amount of $rsETH – a reward-bearing LRT. The $rsETH mirrors the underlying value of the various accrued and initially staked LSTs.

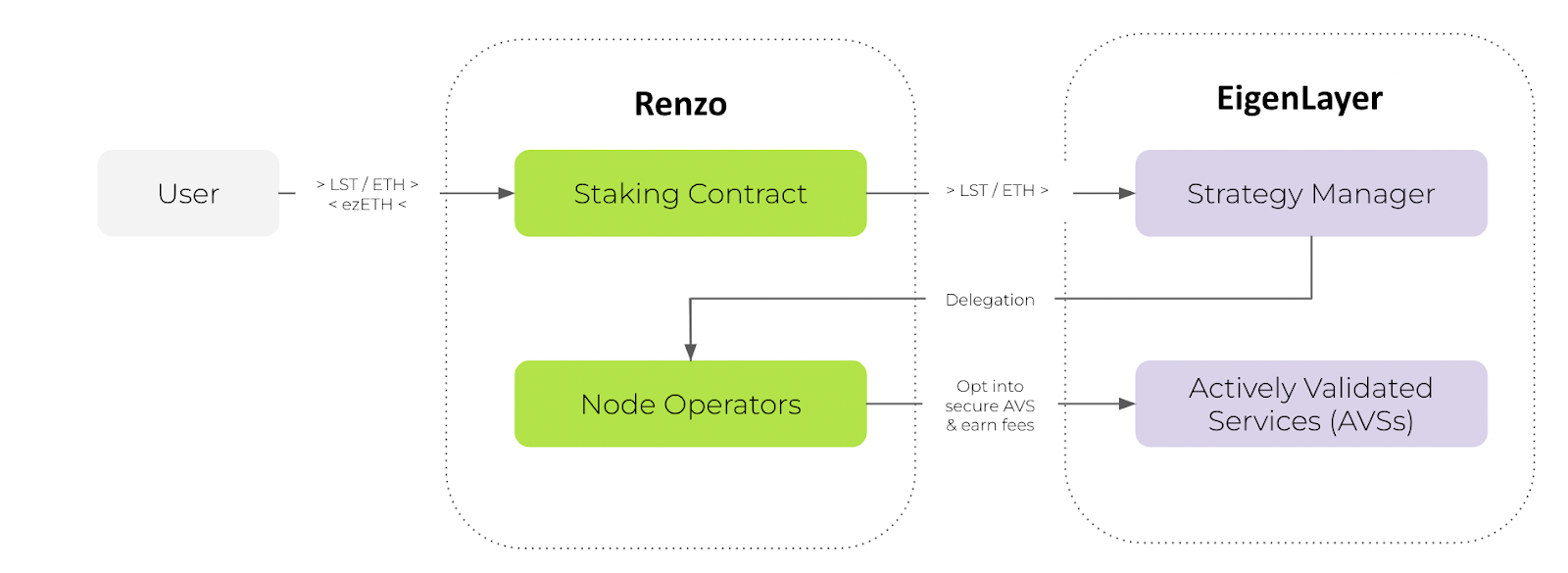

- Renzo Protocol (ezETH) – positions itself as a strategy manager for EigenLayer, operating as a liquid restaking platform. Its primary role involves managing liquid restaking, with a goal to optimize yields and reduce risks for restakers. Analogous to a hedge fund manager in the traditional finance dictionary, Renzo actively manages AVS portfolios by adhering to Markowitz’s efficient portfolio strategy. This approach seeks to achieve the highest possible yield with a balanced level of risk, or alternatively, the lowest risk for the anticipated return. Renzo has adeptly consolidated its services into an LRT called $ezETH. Looking forward, Renzo was built to support any ERC20 token for securing AVSes, not only ETH and LSTs.

- Puffer Finance (pufETH) – a native liquid restaking protocol that prioritizes decentralization, particularly by empowering home stakers, and emphasizes security, featuring anti-slashing measures such as Secure-Signer and RAVe. In Layman’s terms, two key features, Secure-Signer and RAVe, enhance validator security and protect against slashing risks arising from client bugs and operator errors. This reduced risk enables Puffer to work towards a system where operators can validate with as little as 1 ETH in collateral. All these functionalities are encapsulated in their LRT, $pufETH.

- Swell (rswETH) – The liquid restaking token is another innovation from the already successful Swell team within the LST ecosystem. rswETH has undergone a thorough audit by the premier blockchain security firm, Sigma Prime, and benefits from the development support provided by leading DeFi risk management experts at Gauntlet and Chaos Labs. Additionally, it has been developed in collaboration with Actively Validated Services within the burgeoning restaking ecosystem. As an added perk, rswETH holders are treated to zero fees for the first 30 days following its launch.

- Bedrock (uniETH) – is a liquid restaking protocol incubated by RockX that facilitates native restaking with ETH managed through Eigenpod. Such design allows for contract upgrades accommodating future restaking delegation, providing flexibility for implementing versetile strategies for operator delegation and AVS selection.

- Prime Staked ETH (primeETH) – is a fork of KelpDAO created by the Origin Protocol team, who launched a suite of DeFi yield primimtives over the years. In addition to popular LSTs, the platform supports also OETH from OriginDeFi.

Many more innovative strategies are emerging to capture and utilize a slice of the LRT market, especially among protocols that are built atop the incoming restaking DeFi legos. Rest assured, we’ll delve into this topic again with a more DeFi-centered perspective.

Will LRT Become Catalyst For The New DeFi Primitives?

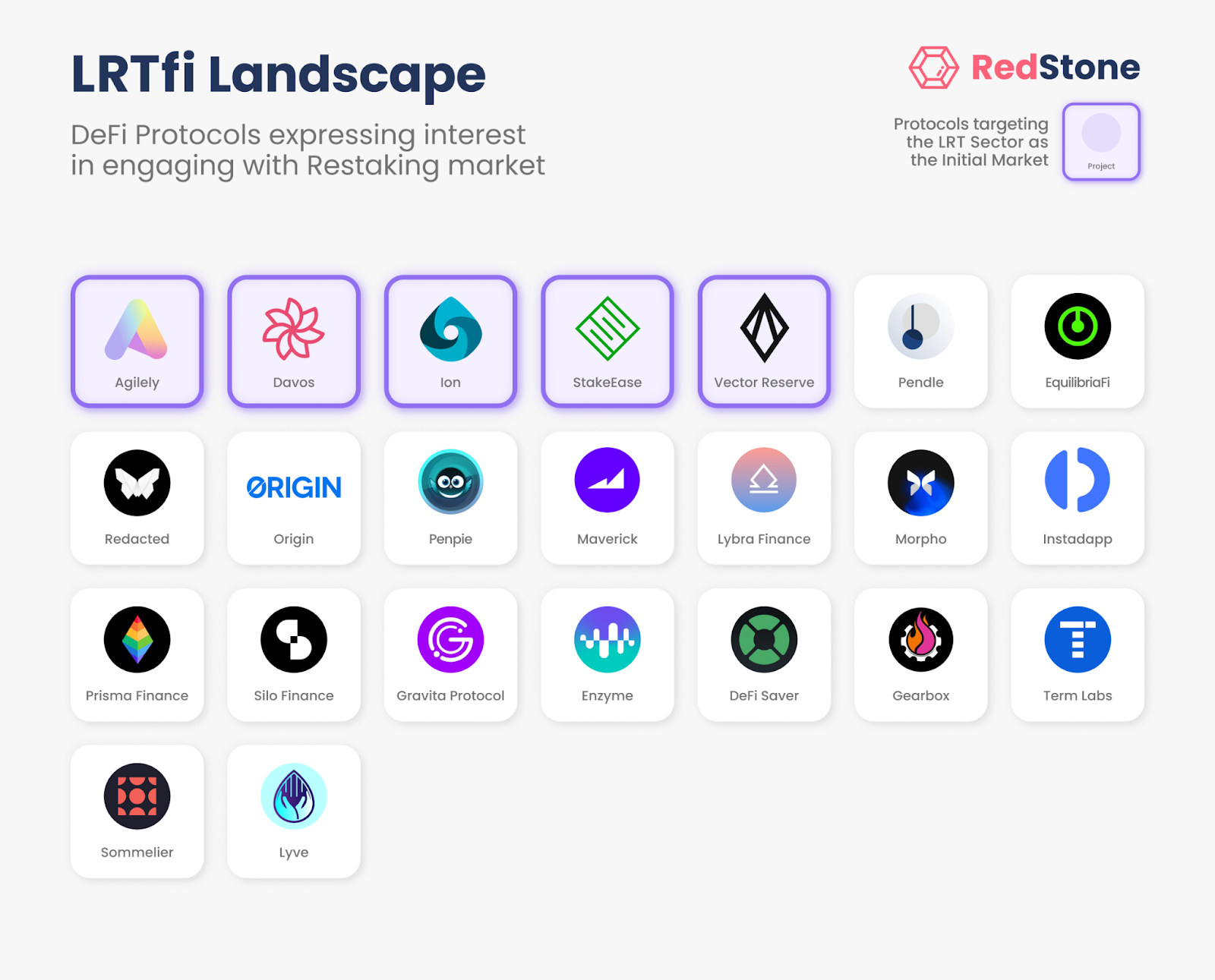

As it often happens when a new DeFi sub-category emerges, numerous developers vie to become the so-called ‘next Uniswap or Aave of X‘. Similarly, we’re witnessing the same market dynamics begin to unfold with protocols built atop restaking primitive. This is exactly how innovation is meant to unfold—through new markets and bold opportunities, particularly as the EigenLayer and LRT space are expected to become an enormous industry and grow exponentially once we fully realize the capabilities of AVSes. Several seasoned protocols are already making strides in integrating and promoting the adoption of LRT within the DeFi landscape. Ultimately, new teams looking to catch this wave of demand will likely seek to secure a first-mover advantage, planning user acquisition campaigns and liquidity initiatives to outperform established players. Here’s a map of all the contenders that have already signed up for the restaking madness, accompanied by brief descriptions of several projects:

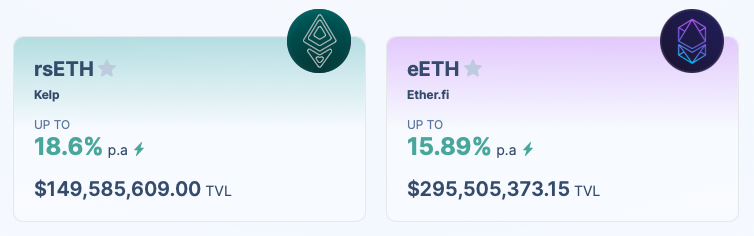

- Pendle Finance, a name already familiar to any enthusiast of LSTfi, is now making significant strides in the LRT domain, with its momentum showing no signs of slowing down. The activities in the LRTfi sphere on Pendle are dynamic and innovative – think leveraged farming and trading based on the future value of EigenLayer’s AVSs, and the anticipated governance tokens of listed LRT. Adding to this excitement, users can not only speculate on the future yields of listed LRT protocols but also engage in additional liquidity initiatives, enabling LRT holders to earn more from the underlying Protocol System’s Points. The prominence of the LRT narrative within Pendle’s ecosystem is evident when we observe that the ether.fi’s $eETH and Keplr’s $rsETH pools are the most heavily capitalized on the platform, boasting TVLs of approximately $295M and $150M, respectively, at the time of writing – a sizeable portion of the underlying TVL. Similar to LSTfi, Pendle proves to be another value-add for LRT protocols looking to bootstrap and deepen their liquidity.

- Penpie – a subDAO under Magpie, is making waves in the Pendle arena. Pendle has adopted the now-classic veTokenomics model pioneered by Curve. Drawing parallels to the infamous Curve Wars, Penpie acts as Pendle’s counterpart to Convex. Holding 11.8 million out of the 42 million total vePendle tokens, which translates to about 36% of the entire supply, Penpie is in a distinct position to leverage the excitement surrounding Pendle’s LRT boom. The dedicated LRT subDAO Eigenpie takes a step further. Its core mechanism enables users to convert their Liquid Staked ETH tokens into Isolated Liquid Restaked ETH tokens via EigenLayer.

- Ion Protocol – is a pioneering lending platform that is price-agnostic, utilizing verifiable validator-backed data to enable users to borrow ETH against their LST and LRT positions. Ion stands at the cutting edge of today’s DeFi innovation with its novel lending framework. All borrowing positions in Ion are price-independent, and their attributes (like interest rates, LTV ratios, position health, etc.) are set based on consensus layer data, bolstered by Zero-Knowledge data systems. Notably, this means liquidations are initiated by shifts in the consensus layer state, not by price movements dictated by oracles. Ion’s approach marks a significant departure towards a unique Beacon-chain-centric design, a path not previously explored in either the LSTfi or any other DeFi sub-category. For a comprehensive understanding of Ion’s mechanisms, do go visit the official docs.

- Redacted Cartel (pxETH) – has recently expanded its horizons with the launch of Pirex ETH, a venture aimed at enhancing Redacted’s vertically-integrated offerings in the staking sector. This includes a comprehensive range of services such as core node infrastructure, RPC services, and most notably, leverage and yield stripping services, all converging to form a cohesive ecosystem embodied in $pxETH – offering one of the highest ETH yields on the market. There are emerging indications that Redacted is gearing up to enter the restaking space, hinted at by the recent news where Blockswap Network delegators voted to integrate $pxETH as LST collateral into the Restaking Cloud.

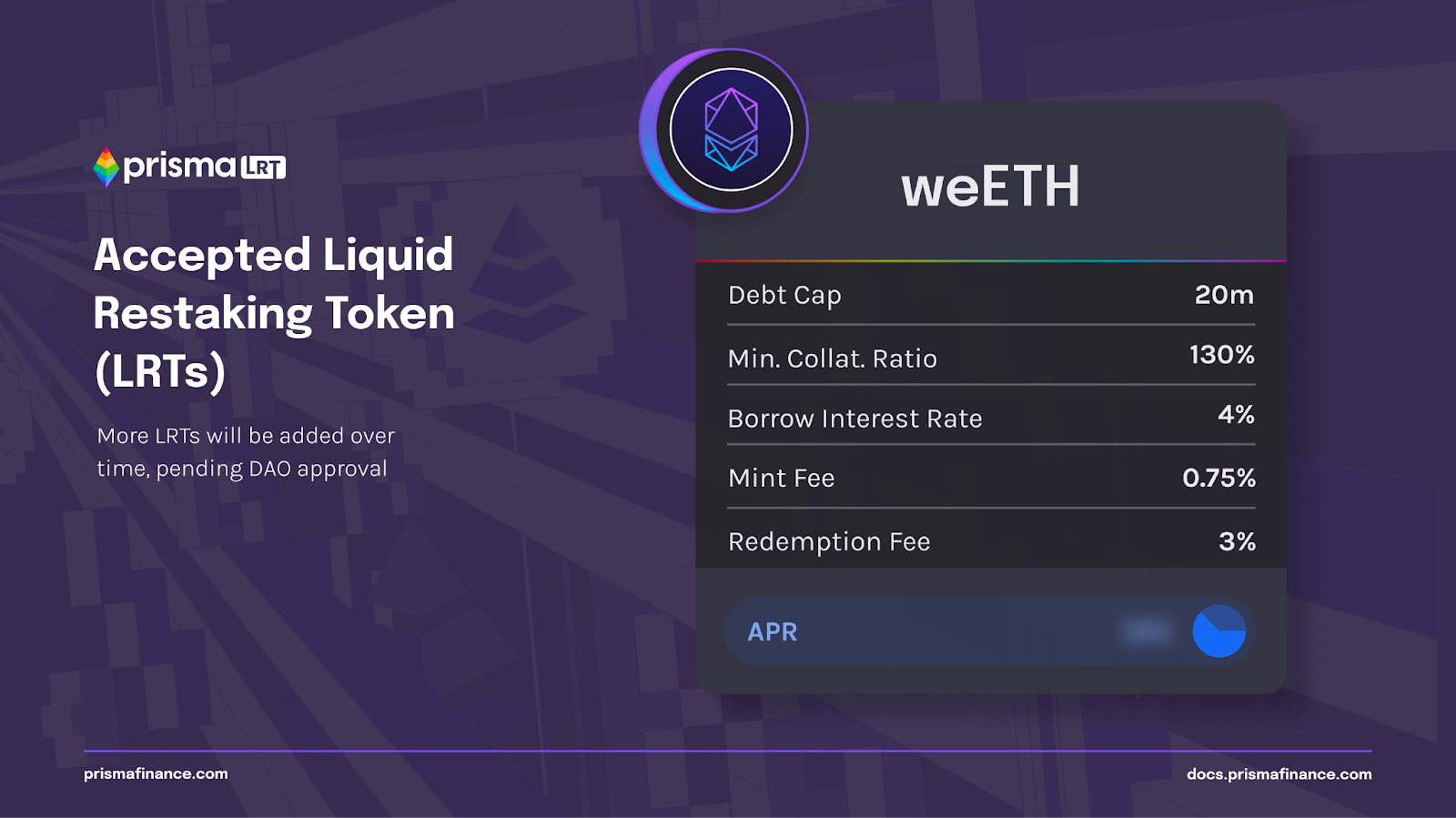

- PrismaLRT – the first LRT-only CDP protocol created by Prisma Finance that enables users to mint the $ULTRA stablecoin using LRTs as collateral (weETH at launch). Specifically designed for LRTs, PrismaLRT integrates directly into the Prisma UI, offering a seamless experience for users looking to borrow using their LSTs or LRTs. By minting $ULTRA with their LRT, depositors can keep all rewards, points, and benefits associated with LRT ownership, while also leveraging ULTRA across the DeFi ecosystem.

- Grativa – a borrowing protocol allowing users to mint $GRAI against their LSTs and LRTs. Gravita decided to streamline the UX and flow for users by bundling both staking and staking tokens into their protocol. The team takes a cosmic theme with the Ascend program leading towards the token launch. Gravita strives to offer more collateral options than the competition, incentivizing more people to use the platform.

- Morpho Blue – a simple and immutable primitive with permissionless market creation, enabling efficient lending of any asset. Notably, the protocol’s flexibility has given rise to one of the first lending markets for LRTs. The platform allows separating risk management from the immutable core protocol, bringing flexibility to the lending sector.

- Silo – a permissionless and risk-isolated lending markets protocol. Lenders deposit funds into an isolated lending market consisting of i.e. weETH and the bridge asset only. If another token like stETH experiences an exploit, weETH lenders will not be affected since the risk is isolated to the weETH market only. Silo has been one of the fastest lending markets to adopt LRTs and is committed to expanding in that category.

What could users expect next in the LRTfi market? It’s visible already: expansion to L2s.

The best example is the Pendle LRT Train on Arbitrum. It allows LRT holders to boost their yield, speculate on the value of points accredited by LRT protocols and implement versatile Yield Token strategies (soon available on other lending markets too).

Where Is EigenLayer and Restaking Ecosystem Heading Towards?

Many regard EigenLayer as the most pivotal project in the crypto landscape since the advent of smart contract capabilities. It indeed offers unmatched potential, especially in the realm of crypto-economic design. This includes simplifying the intricacies of establishing a decentralized validator set and leveraging the most secure, permissionless network to date for new ventures. This enables builders to concentrate solely on innovating at the application layer

We’ve recently observed the strength of the restaking narrative, as evidenced by the EigenLayer ecosystem breaking through the $7.5 billion TVL barrier and the Ether deposits in LRT protocols that are live on the mainnet skyrocketing.

As the value locked within EigenLayer predominantly rises, we are witnessing exponential growth in airdrop-driven economics. As highlighted, nearly every LRT protocol features its unique point system, such as ether.fi points, Kelp’s miles, Renzo ezPoints and Puffer’s carrots – all built on top of the enticing promise of allocations within the EigenLayer protocol. Moreover, a flourishing DeFi ecosystem is emerging, grounded on the prospect of such airdrops, including platforms like whales.market and more sophisticated derivatives like Pendle’s YT tokens. The significant challenge for EigenLayer is to transcend the frenzy of airdrops and establish a sustainable, genuine yield-generating ecosystem, fueled by the supply and demand dynamics between ETH restakers and AVSes.

While this may seem far-fetched and detached from today’s crypto reality, EigenLayer is scheduled to launch on Mainnet in Q2 of this year, and some AVSes, like EigenDA, are anticipated to debut within this very quarter!

We can’t conclude a discussion about EigenLayer without addressing some of the criticisms it faces, such as concerns about what occurs during a cascade liquidation event, or the potential risk of restaking overloading the Ethereum consensus. There are valid arguments on both sides, and the general consensus is that we’ll need to observe how things unfold in practice. Nonetheless, if anyone is equipped to create an open, decentralized, and universal trust marketplace, the EigenLayer team appears to be the most suitable candidate for the task.

However, despite its abstract nature, the LRT ecosystem, and more broadly, the EigenLayer landscape, must still adhere to the existing laws of crypto physics. This means constructing a DeFi flywheel by enhancing token utility throughout the system, ensuring that a price oracle for LRT is accessible to all in a low-latency, highly secure manner, and boosting LRT liquidity to minimize slippage. Interestingly, the only ERC20 tokens supported for restaking are LSTs for now. But in the future, AVSes will be able to choose any ERC20 token or any combination of i.e. ETH + LSTs + ERC20 tokens to use for securing the AVS. As a result, networks like Celo will be able to secure their AVS with the native token in combination with ETH and potentially give higher rewards to native token holders.

LRT Landscape Q1 2024

At RedStone, we’re closely monitoring the Restaking landscape and are committed to supporting the ecosystem with cost-efficient data feeds: see LRTs RedStone supports in Push model and LRTs RedStone supports in Pull model.

Keep an eye on the RedStone Twitter account for updates – something is in the works, and we’ll soon reveal what we’ve been developing within the Liquid Restaking Ecosystem 👀

Disclaimer: This post is not a financial advice. It was created for informational purposes only. Remember to always do your own research.

About RedStone

RedStone is a modular oracle delivering diverse, high-frequency data feeds to EVM Layer1, Layer2, Rollup-as-a-Service networks and beyond, i.e., Starknet, Fuel Network, or TON. By responding to market trends and developer needs, RedStone can support assets not available elsewhere. The modular design allows for data consumption models adjusted to specific use cases, i.e., capital-efficient LSTfi and early support of LRTs. RedStone raised almost $8M from Lemniscap, Blockchain Capital, Maven11, Coinbase Ventures, Stani Kulechov, Sandeep Nailwal, Alex Gluchovski, Emin Gun Sirer, and other top VCs & Angels.